Halving: Market Prospects

The recent weekend halving was marked by a commission race for block 840,000, which earned miners 3.125BTC and was accompanied by over 40BTC in fees, demonstrating how miners’ motivations could evolve in the future. Halving is a programmed process, anticipated by the market every 210,000 mined blocks (approximately every four years), where miners’ rewards are halved. In previous posts, we noted how issuers of BTC spot ETFs profit from revaluing their investments in public crypto companies—this logic partly explains market price movements for a comfortable mining operation mode.

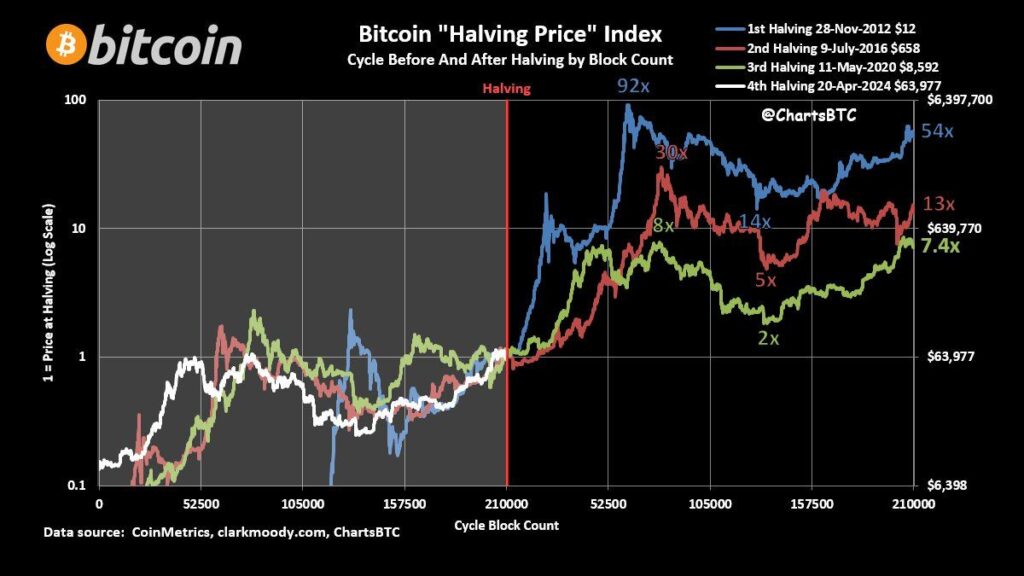

Historical price analysis suggests a potential rise in BTC value following a halving of organic supply. Observations indicate that in previous periods, prices increased two to ninety-two times over the next four years, depending on the cycle and BTC’s initial market cap. This insight into the potential market trajectory can be invaluable for investors, miners, and analysts.

The current industry landscape has undergone significant changes. BTC has achieved a high level of market adoption, with numerous exchange products launched in the US and EU. The trading volume of BTC options and futures nearly doubled last year, with prices reaching historical highs. Public reports from mining companies in the US offer valuable insights into the sector’s outlook and help shape baseline expectations for future supply and demand scenarios. This context is crucial for understanding the potential implications of the halving on Bitcoin’s market prospects.

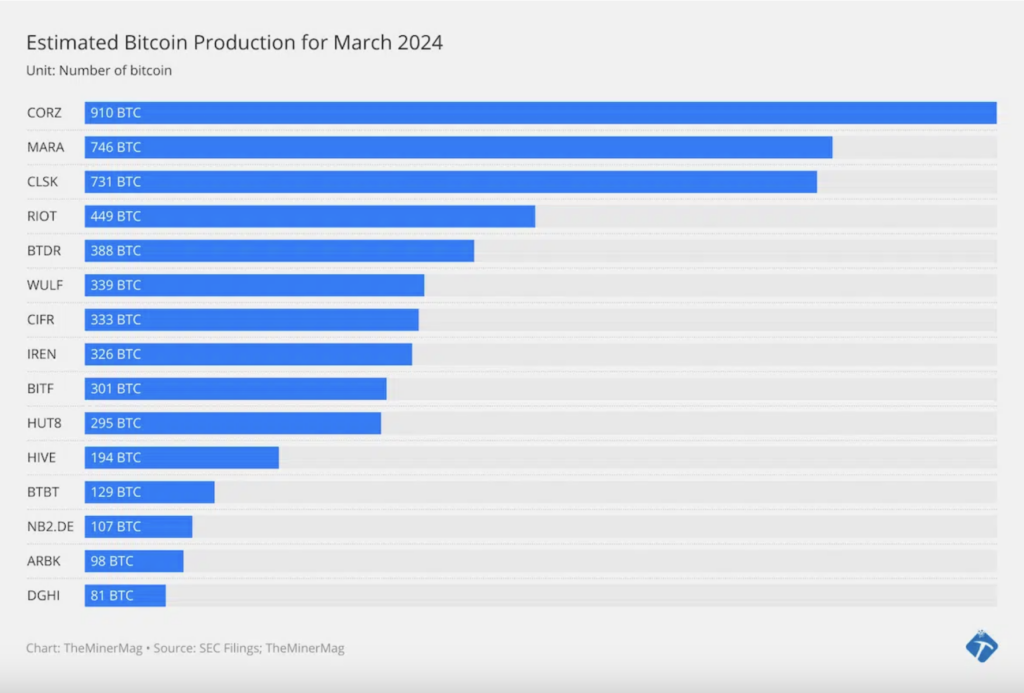

Miners are expected to mine about 13,500 BTC monthly, with approximately 20% attributed to public mining companies in the US. The main buyers in the market are investment companies, banks, and ETF issuers, and at the current price of 64,000 per BTC, around 8 million USD in daily liquidity inflow is required to purchase all the BTC mined in this way. According to Farside, the current average inflow for spot ETFs on the American market is 177 million USD, theoretically covering not only the public but also the private mining sectors and speculative profit taking by other market participants.

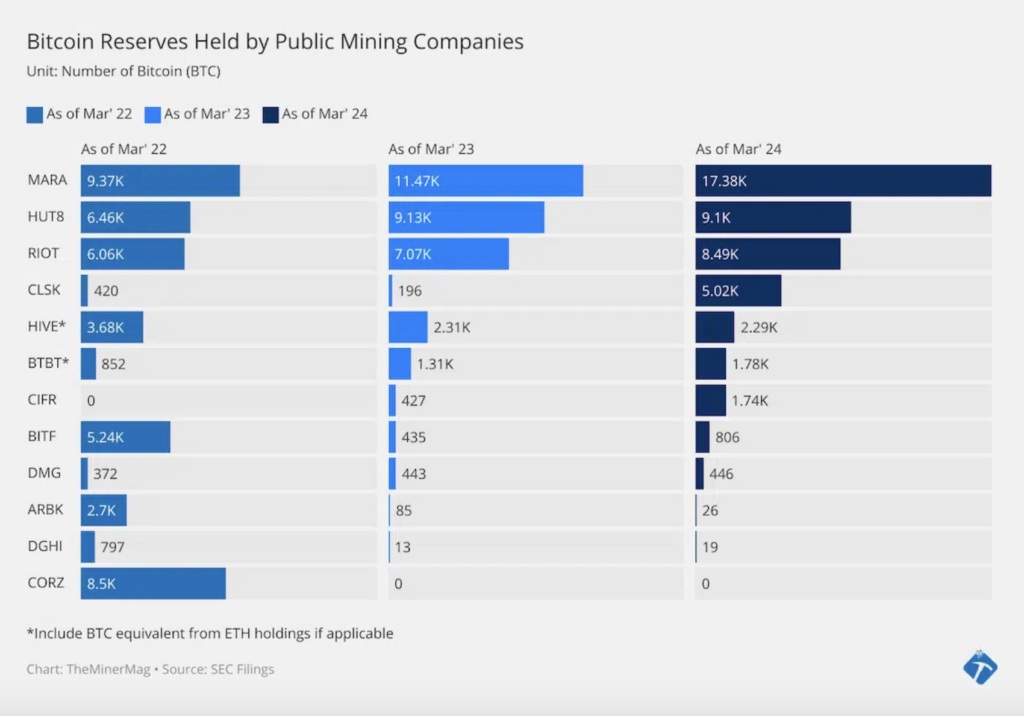

However, data shows that not all miners prefer to realize profits immediately. Most public participants accumulate BTC portfolios, on the one hand supporting current prices by reducing supply and anticipating future growth, and on the other hand, building reserves for a positive revaluation of their stocks. Sales of BTC from the balance sheets of the leading mining volume company, Core Scientific (CORZ), are linked to the need to pay off debts as part of creditor protection procedures. Still, this company also plans to increase capacities and build up reserves.

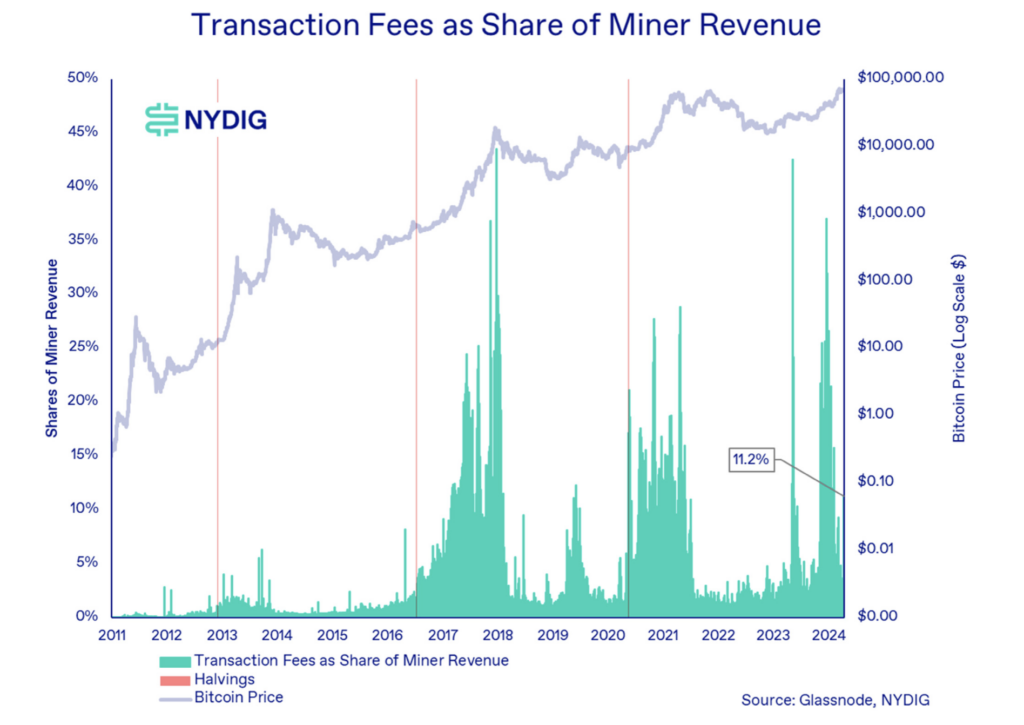

An alternative way for miners to profit could be through transaction fees. Previously, such revenue increased during periods of high demand for BTC, but recently, sources of increased commissions come from new protocols using blockchain space to store external information—text records, audio, and video. Projects like Ordinals or Rune attract users and liquidity by creating tools for “eternal storage” of information and secondary markets for speculative ownership of such tokens. However, the sustainability of this trend and how it will be affected by competition with L2 solutions for the main network (such as rootstock, stacks, mezo, etc.) remains a big question.