Liquidity in Cryptocurrencies: How Money Flows and Cryptocurrency Trading Work

Two liquidity contours can be identified in the cryptocurrency market —the first related to fiat currencies, and the second associated with stablecoins, bitcoin, Ethereum, and other altcoins.

The first contour includes:

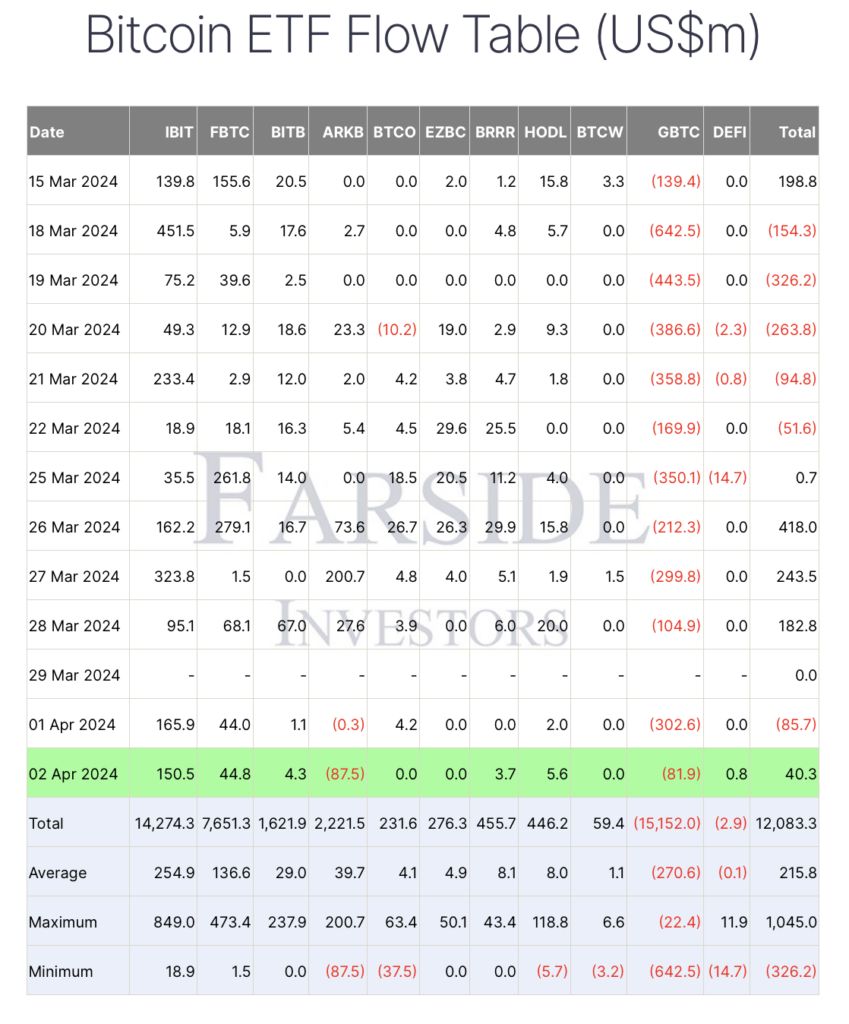

- Inflows into ETFs or ETPs.

- Trading in shares of public crypto companies.

- The injection of funds into exchanges through payment companies or in a p2p format.

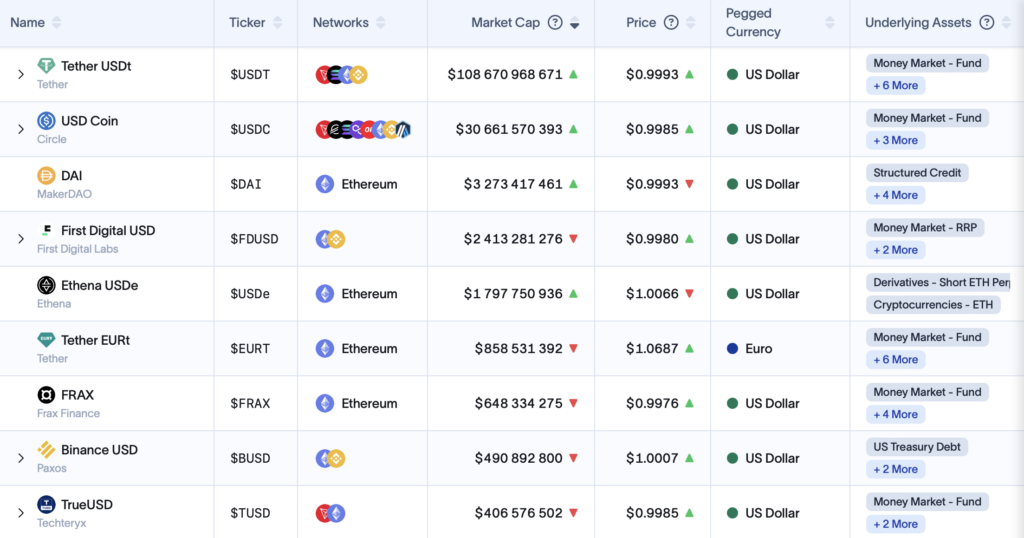

The second contour consists of stablecoins from crypto companies that have contact with traditional markets – USDC, USDT, PYUSD, etc., and stablecoins backed by cryptocurrency collateral – crvUSD, DAI, FRAX, etc.

Wherever there is a liquidity transfer, there is a fee for speed and convenience and interest on balances or deposits. The fee for providing liquidity is often associated with centralized or decentralized loans.

Apart from the flows related to buying/selling in the spot market, specific speculative liquidity is associated with derivative trading – buying and selling options and futures. The connection between different trading platforms, hours of activity, and the type of market characterizes this liquidity category. The volume of liquidity in buy and sell orders in spot markets correlates with the volume of open interest in derivatives (futures and options), adjusted for the operating hours of traditional exchange platforms, especially in the American markets.

As a result, when assessing the direction of liquidity flow movements, a complex composition emerges consisting of the volume in the order books of crypto exchanges, trading flow in major crypto stocks on traditional platforms, the volume of new stablecoin issuance, and rates in the “crypto money market,” all dissected across spot, futures, and options markets.

Overall, the demand for crypto liquidity is high for financing trading and investments and as collateral for loans. However, the cost of money varies and depends on the form and platform of placement.

Let’s break down how returns in these markets work.

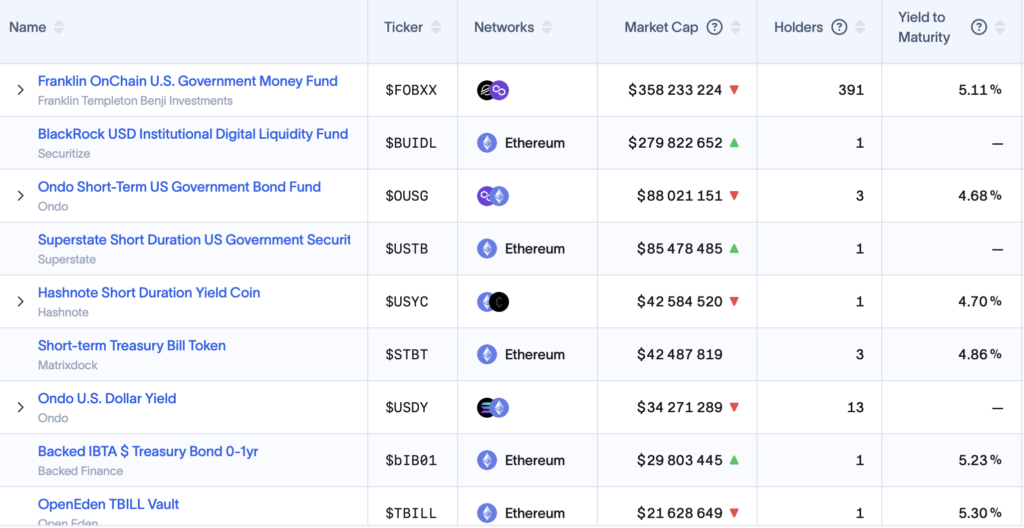

The basis of crypto dollar returns is the investment of collateral dollars in securities, usually bonds, and most often short-term Federal Reserve bonds. The rate is 5.2%. Simplified, you transfer USD to an offshore account and receive USDT, and the Tether company invests them in short-term bonds. Currently, the rate is relatively high, whereas a couple of years ago, it was near zero. But it’s still enough for the issuers to live on.

Some investment companies, like Franklin Templeton or Wisdom Tree, execute a reverse maneuver—they accept stablecoins like USDT/USDC and convert them back into USD, which is then invested in the US bond market. The returns are paid within their app in a tokenized form through an offshore company—a kind of tax optimization with elements of investment returns within the framework of testing market concepts of “tokenize everything.”

In crypto, the yield for over-collateralized stables is ensured through marketing budgets, proceeds from exchange pools on decentralized exchanges, or lending services.

But what if you want to do more than buy Bitcoin for your portfolio and earn from its revaluation? In this case, there are several options for action that take into account the movement of crypto liquidity at different levels:

Arbitrage and “pair trading” between correlational assets is one option. The most striking example we recently discussed in the channel is closing the valuation gap between the base asset (BTC) and a related asset – for example, shares of Coinbase or Microstrategy. This method involves risks – the gap can persist for a very long time and even increase significantly if options can trigger a gamma squeeze on sellers or force leveraged buyers into liquidation.

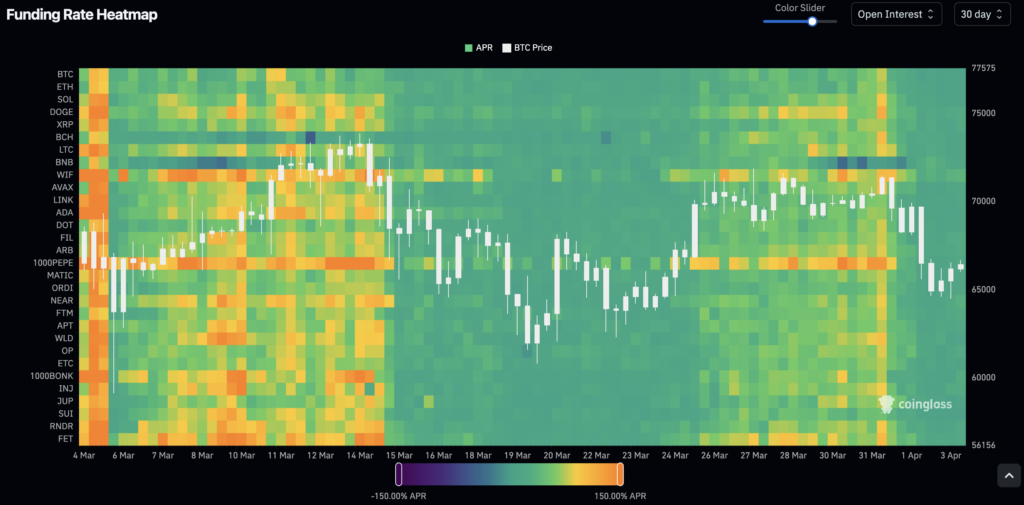

The second method involves collecting the funding rate or yield rate in calendar spreads. Due to the large number of leveraged transactions, there is often an increased demand for specific futures contracts or borrowed liquidity. For example, rates for such deals reached up to 30% per annum in March.

Another option is the use of options strategies – either pre-made or self-developed.